Low-Carbon Hydrogen Development Program Sanctioned and Published

The Brazilian Federal Government has enacted and published Law No. 14.990/2024, which establishes the Low-Carbon Hydrogen Development Program (PHBC), in line with similar international policies such as the US Inflation Reduction Act and the REPowerEU. This follows in the footsteps of Law No. 14,948/2024, which established the Low-Carbon Hydrogen Legal Framework in Brazil.

PHBC is intended to provide financial subsidies through the concession of tax credits to certain low-carbon hydrogen projects. The program was initially addressed in the Bill of Law which resulted in Law No. 14,948/2024, but the statute was vetoed by the President as it failed to indicate which specific tax would be reduced by the tax credits. Law No. 14.990 expressly indicates that the tax credits will reduce the Social Contribution on Net Profit.

See our publications on the Law No. 14.948/2024 in the Brazil Energy Journal and in the Insight.

PHBC Purposes:

The purposes of the PHBC, which will be taken into account during the concession of the credits, are to:

I – Develop the Low-Carbon Hydrogen and Renewable Hydrogen, as defined in Article 4, Items XII and XIII of Law No. 14,948/2024;

II – Support energy transition actions;

III – Set targets for the development of the low-carbon hydrogen internal market;

IV – Apply incentives to decarbonize the hard-to-abate sectors of the economy, such as fertilizers, steel, cement, chemicals and petrochemicals by using low-carbon hydrogen; and

V – Promote the use of low-carbon hydrogen in heavy transport.

PHBC Mechanism:

PHBC tax credits will apply for the supply of low-carbon hydrogen and its derivatives produced in Brazil and will be equivalent to up to 100% of the difference between the estimated price of low-carbon hydrogen and the estimated price of substitute products to increase competitiveness of the low-carbon hydrogen and derivatives, subject to upcoming regulations.

The percentage of tax credit may be inversely proportional to the greenhouse gas (GHG) emission intensity of the produced hydrogen, and will be subject to a competitive process as explained below.

Eligibility Criteria:

Projects must meet at least one of the following criteria to claim tax credits under the PHBC:

I - Contribute to regional development;

II - Contribute to climate change mitigation and adaptation measures;

III - Encourage technological development and diffusion; or

IV - Contribute to the diversification of the Brazilian industry.

PHBC Tax Credits:

Limits:

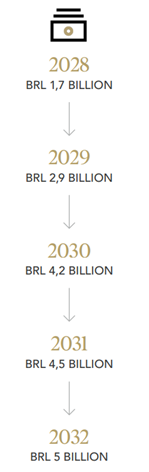

Law No. 14.990/2024 establishes the following annual limits for the granting of tax credits:

The executive branch will determine the value of the tax credits in accordance with the fiscal goals and PHBC’s objectives, which will be included in the annual federal budget. Tax credits within the annual limits that are not used in a given calendar year may be used in subsequent years.

Competitive Process Publicity and Criteria:

The tax credits shall be allocated to producers or purchasers of low-carbon hydrogen through a competitive process. The amounts of tax credits and the corresponding beneficiaries will be disclosed by the executive branch.

One of the selection criteria of the competitive process will be the lowest value of the credit per unit of measurement of the product.

Qualification Requirement:

To participate in the competitive process, producers that are, or were, beneficiaries of the Special Incentive Regime for the Production of Low Carbon Hydrogen (Rehidro), pursuant to Articles 26 to 29 of Law No. 14,948/2024; and purchasers that acquire Low Carbon Hydrogen produced by a company or consortium of companies that are beneficiaries of Rehidro.

The qualification phase will not exceed 90 days.

Further Regulation:

The regulation of the competitive process may also provide for:

I – The allocation of tax credits in decreasing amounts;

II – Priority for projects that: a) have the lowest intensity of GHG emissions from the hydrogen produced or consumed; and b) have the greatest potential for developing the national value chain;

III – The determination of the among of the tax credit based on the difference between the price of the hydrogen and the price of substitute goods;

IV – Submission of guarantees to secure the implementation of the project; and

V – Imposition of penalties.

Penalties:

If the winning project is not implemented—or is implemented in violation of the laws or regulations—the tax credit beneficiary will be subject to:

(i) A fine not exceeding 20% of the value of the tax credit that would have been allocated to the project under the terms of the regulations; and

(ii) Payment of the amount equal to the tax credits unduly refunded or offset, or the cancellation of the tax credits, by the last business day of the month following the month in which the project has violated the laws or regulations.

Social Contribution on Net Profit:

PHBC tax credits correspond to credits of the Social Contribution on Net Profit. The amount of the tax credits will be included in the operating income.

Tax credits shall consist of either:

I - Offsetting of debts, due or overdue, related to taxes imposed by the Ministry of Treasury's Special Secretariat for Federal Revenue of Brazil; or

II - Reimbursement in cash.

If the tax credit has not been offset, the Special Secretariat for Federal Revenue of Brazil shall reimburse the beneficiary within 12 months from the date of the request.

The tax credits may be granted only for low-carbon hydrogen or its derivatives produced in the national territory from January 1, 2028 to December 31, 2032.

Annual Low Carbon Hydrogen Policies Report

The Executive Branch will publish an annual report with the evaluation and results of the National Low Carbon Hydrogen Policy, the PHBC, the Brazilian Hydrogen Certification System (SBCH2) and Rehidro.

The annual report will also include a list of projects that have claimed for the tax credits, the qualified projects and the results of the monitoring and inspection actions of the PHBC and the National Low Carbon Hydrogen Policy, as well as any imposed administrative penalties and fines.

National Low Carbon Hydrogen Policy

Law No. 14.990/2024 establishes that the Ministry of Mines and Energy (MME), will propose to the National Energy Policy Council (CNPE):

I – the technical and economic parameters for drawing up the foundations of the National Low Carbon Hydrogen Policy; and

II – the work plan for the implementation, supervision and evaluation of the instruments of the National Low Carbon Hydrogen Policy, such as National Hydrogen Program (PNH2), PHBC, Rehidro, among others, which shall be prepared within 90 days counted from the date of the publication of law.